Biweekly Mortgage Calculator

Modern scientific illustration of Biweekly Mortgage Calculator

Modern scientific illustration of Biweekly Mortgage Calculator

Biweekly Mortgage Calculator: Pay Off Your Home Faster & Save Thousands on Interest

Buying a home is likely the single largest investment you will ever make. It is also the largest debt you will ever carry. When you look at your standard 30-year mortgage agreement, the numbers can be terrifying. Over the life of a loan, you might end up paying nearly as much in interest as you did for the house itself.

But what if there was a simple mathematical strategy to slash years off your mortgage term and keep thousands—potentially tens of thousands—of dollars in your pocket instead of handing it over to the bank?

Enter the Biweekly Mortgage Calculator.

Most homeowners default to the standard monthly payment plan simply because that’s what lenders present. However, switching to a biweekly payment schedule is one of the most powerful "hacks" in personal finance. This tool isn't just a calculator; it is your roadmap to financial freedom.

In this guide, we will explore exactly how our best-in-class Biweekly Mortgage Calculator works, the math behind the savings, and how you can use it to build equity at record speed.

What is a Biweekly Mortgage Calculator?

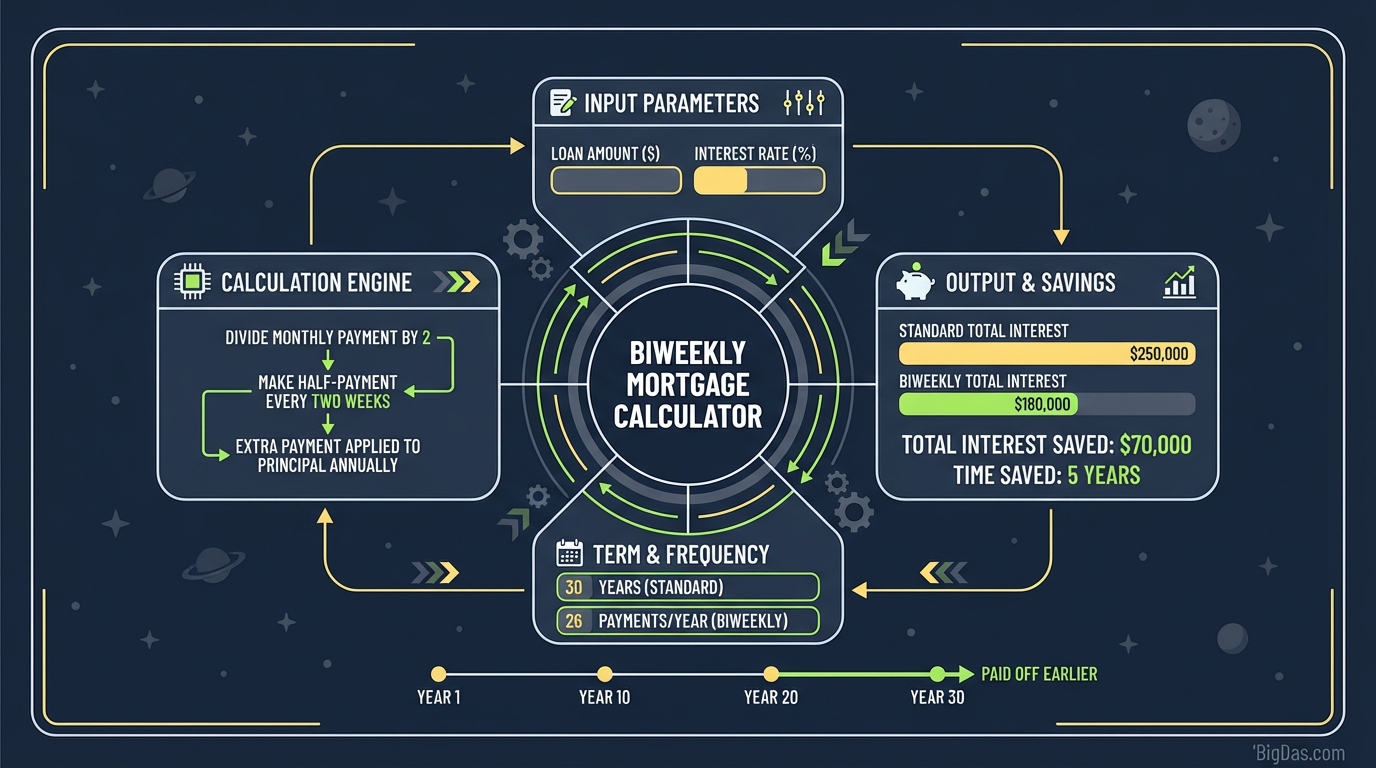

To understand the tool, you must first understand the strategy. A Biweekly Mortgage Calculator is a digital financial tool designed to compare the outcome of making standard monthly mortgage payments versus making payments every two weeks.

The Math Behind the Magic

Here is the fundamental difference that most borrowers miss:

- Monthly Payments: There are 12 months in a year. If you pay once a month, you make 12 full payments annually.

- Biweekly Payments: There are 52 weeks in a year. If you pay every two weeks, you make 26 half-payments.

Here is where the math gets interesting. Since 26 half-payments equal 13 full monthly payments, the biweekly schedule effectively forces you to make one extra full mortgage payment every year.

However, because that extra money is applied directly to your principal balance (not the interest), it reduces the amount of interest charged in subsequent months. This creates a snowball effect that dramatically shortens the amortization schedule of your loan.

Our calculator visualizes this accelerated payoff, showing you exactly when you will be debt-free.

Key Features & Benefits of Our Tool

Not all mortgage calculators are created equal. Many generic tools simply estimate basic interest. Our Biweekly Mortgage Calculator is engineered to be the most accurate and user-friendly tool on the market, handling complex amortization variables with ease.

1. Precision Savings Analysis

We don’t just show you the monthly difference; we calculate the Total Interest Saved down to the penny. You will see exactly how much richer you will be by switching schedules.

2. Time-Saved Visualization

Money isn't the only currency; time matters too. Our tool calculates exactly how much time you shave off your mortgage term. Imagine owning your home free and clear 4, 5, or even 7 years earlier than planned.

3. Side-by-Side Comparison

The tool generates a dual-view report. On the left, your current "Standard Monthly" trajectory. On the right, your "Biweekly Accelerated" trajectory. This immediate visual contrast makes the decision simple.

4. Interactive Amortization Graphs

Static numbers can be boring. Our tool features dynamic charts that show your equity growing faster and your interest shrinking steeper compared to a standard loan.

5. Inflation and Future Value Consideration

By paying off debt early, you mitigate the risk of future financial instability. Our tool helps you plan for a secure future by highlighting the accelerated growth of your home equity.

How to Use the Biweekly Mortgage Calculator (Step-by-Step)

Getting accurate results takes less than 30 seconds. Follow this guide to unlock your savings potential.

Step 1: Gather Your Loan Details

To get the most precise output, grab your latest mortgage statement. You will need:

- Current Principal Balance

- Interest Rate

- Remaining Loan Term (or original term and start date)

Step 2: Input Your Data

Enter your numbers into the calculator fields:

- Loan Amount: Enter the original amount or current balance.

- Interest Rate: Enter your annual percentage rate (e.g., 6.5%).

- Loan Term: Select 30 years, 15 years, or a custom length.

- Start Date: Select when the payments began (to see historical data) or start from today.

Step 3: Analyze the "Accelerated" Results

Once you hit calculate, focus on these three metrics generated by the tool:

- New Payoff Date: Mark this on your calendar. This is your new "Freedom Date."

- Total Interest Saved: This is the amount of money you are effectively earning by changing your payment method.

- True Biweekly Payment: This shows you the exact amount you need to budget every two weeks.

Step 4: Review the Amortization Schedule

Scroll down to the detailed table. Look at how quickly the "Principal" portion of your payment increases compared to the "Interest" portion. In a standard loan, the first few years are almost entirely interest. With the biweekly approach, you start chipping away at the principal immediately.

Why You Need This Tool: Top Use Cases

Who benefits most from the Biweekly Mortgage Calculator? Practically anyone with a home loan, but specifically these groups:

1. The New Homeowner

If you just signed a 30-year mortgage, you are in the best position to save. Interest is front-loaded on mortgages. Implementing a biweekly strategy from Year 1 maximizes the compound savings effect. Use this tool to set your strategy before you make your first payment.

2. The Refinancer

If you recently refinanced to get a lower rate, do not just pocket the savings. Use this calculator to see what happens if you apply that lower rate to a biweekly schedule. You could potentially turn a 30-year refinance into a 22-year payoff without feeling a pinch in your budget.

3. The Retirement Planner

If you are 45 years old with 25 years left on your mortgage, you might be carrying debt into retirement. This tool can show you how to eliminate that mortgage before you retire, significantly reducing your monthly expenses when you move to a fixed income.

4. The Equity Builder

Planning to sell in 5 to 7 years? By using the biweekly method, you will have paid down significantly more principal by the time you sell. This means a larger check for you at closing, which can be used for a larger down payment on your next dream home.

Strategic Advice: Getting the Most Out of Biweekly Payments

While the calculator shows you the math, execution is key. Here are expert tips on how to implement this strategy effectively after using our tool.

Check with Your Lender First

Not all servicers accept biweekly payments directly. Some may hold your partial payment until the second half arrives, negating the interest savings. You need to ensure your lender applies the payment upon receipt.

Beware of Third-Party Fees

Some companies charge a setup fee or a transactional fee to manage biweekly withdrawals for you. Do not pay this. You can achieve the same results for free.

The "DIY" Biweekly Method

If your bank is difficult, you can simulate the biweekly effect yourself:

- Use our calculator to find out what your biweekly total adds up to annually.

- Divide your monthly payment by 12.

- Add that amount to your regular monthly payment designated as "Principal Only."

- This achieves the exact same mathematical result (13 payments a year) without changing your withdrawal schedule.

Frequently Asked Questions (FAQ)

1. Does biweekly payments really save money?

Yes, absolutely. By making payments every two weeks, you make 26 half-payments a year, which equals 13 full payments. This reduces your principal balance faster, meaning interest is calculated on a smaller amount each month. On a typical $300,000 loan, this can save over $30,000 to $50,000 in interest depending on rates.

2. Will my lender charge me for switching to biweekly payments?

Some lenders charge a setup fee to alter your auto-draft schedule. However, most major banks are becoming more consumer-friendly and allow this for free. Always ask if there are administrative fees before signing up for their official program.

3. Can I use this calculator for an existing mortgage?

Yes. Simply input your current mortgage balance rather than the original loan amount, and input the remaining term. The tool will show you how much money and time you can save starting from today.

4. Is biweekly better than a 15-year mortgage?

A 15-year mortgage usually offers a lower interest rate but requires a much higher mandatory monthly payment. A biweekly strategy on a 30-year loan offers flexibility; you are paying off the loan faster, but you are not contractually obligated to the higher monthly sum if you run into financial hardship (provided you manage the payments manually).

5. Why doesn't the bank suggest this automatically?

Banks are businesses. They make profit through interest. While they are happy to lend to you, it is not in their profit-margin interest to help you pay off the loan early. You must take the initiative to set this up.

Conclusion: Take Control of Your Mortgage Today

The difference between a 30-year mortgage and a 24-year mortgage isn't just time—it’s freedom. It’s money in your retirement account, funds for your children’s education, or the capital for your next investment property.

Don't let your mortgage run on autopilot. The standard monthly plan is designed to maximize the bank's profit, not your wealth. By using our Biweekly Mortgage Calculator, you are taking the first step toward flipping the script.

The numbers don't lie. A small adjustment to how you pay can lead to massive changes in what you own.

Ready to see how much you can save? Scroll up, enter your loan details, and uncover your path to a mortgage-free life.