Loan Calculator

Modern scientific illustration of Loan Calculator

Modern scientific illustration of Loan Calculator

The Ultimate Loan Calculator: Estimate Payments, Analyze Interest, and Master Your Debt

Taking out a loan is one of the most significant financial decisions you will make in your lifetime. Whether you are closing on your dream home, financing a new vehicle, or consolidating credit card debt with a personal loan, the numbers matter.

A fraction of a percentage point in interest or a slight adjustment to the loan term can mean the difference of thousands—sometimes tens of thousands—of dollars over the life of the loan.

Yet, many borrowers enter agreements looking only at one number: the monthly payment. While affordability is crucial, it is only part of the story. To truly master your finances, you need to understand how that payment is structured, how much is vanishing into interest, and how quickly you are building equity.

Enter our Best-in-Class Loan Calculator. This isn't just a simple adding machine; it is a financial simulation engine designed to give you clarity, confidence, and control over your borrowing.

Below, we dive deep into how this tool works, the critical difference between principal and interest, and how you can use this calculator to save money and get out of debt faster.

What Is a Loan Calculator? (Beyond the Basics)

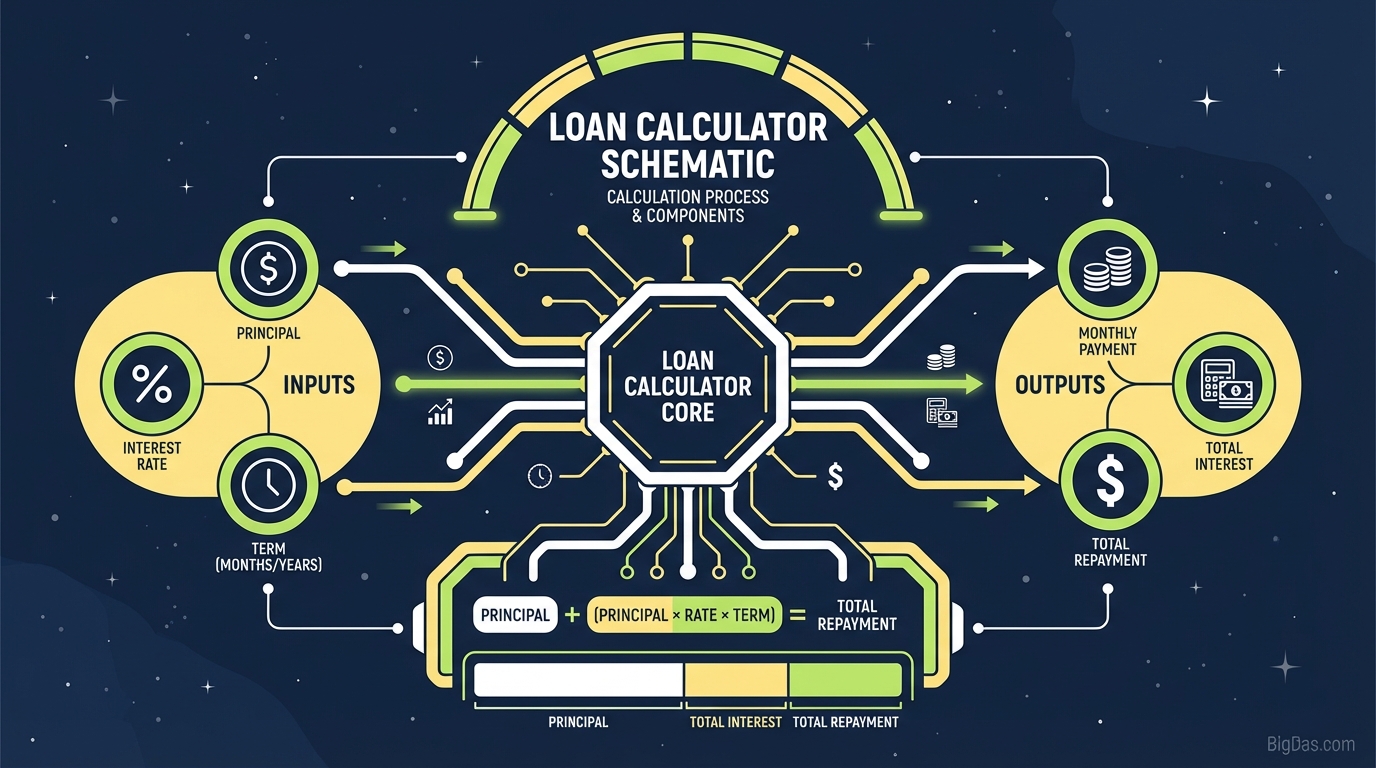

At its core, a Loan Calculator is a digital utility that computes the periodic payment amount necessary to pay off a loan based on three primary variables: the principal, the interest rate, and the loan term.

However, to understand the value of this tool, you must understand the financial concept it automates: Amortization.

Understanding Amortization

Most loans (mortgages, auto loans, personal loans) are "amortized." This means your monthly payment remains the same for the entire duration of the loan, but the composition of that payment changes every single month.

- Early in the loan: The majority of your payment goes toward Interest (profit for the lender). Very little goes toward reducing your debt.

- Later in the loan: The scales tip. The majority of your payment goes toward Principal (the money you actually borrowed).

Our Loan Calculator does the complex algorithmic heavy lifting to generate an Amortization Schedule instantly. It peels back the layers of your monthly bill to show you exactly where your money is going.

Why Mental Math Doesn't Work

You cannot simply take a $10,000 loan at 5% interest and assume the total repayment is $10,500. Because interest compounds and is calculated on the remaining balance monthly, the math requires complex formulas. Our tool eliminates the risk of human error, providing bank-level accuracy in milliseconds.

Key Features & Benefits of Our Loan Calculator

Why is this specific tool considered the industry standard for borrowers? It combines ease of use with deep analytical power.

1. The "Principal vs. Interest" Breakdown

This is the most critical feature for financial planning. The tool visualizes the split between what you borrowed and the cost of borrowing.

- Benefit: You might realize that extending a car loan from 4 years to 7 years lowers your monthly payment by $50, but costs you $2,000 more in total interest. This feature helps you make the smartest long-term decision, not just the easiest short-term one.

2. Multi-Loan Versatility

Our calculator is agnostic to the loan type. It uses the standard amortization formula applicable to:

- Mortgages: Fixed-rate home loans (15, 20, or 30 years).

- Auto Loans: New or used vehicle financing.

- Personal Loans: Unsecured loans for travel, weddings, or debt consolidation.

- Business Loans: Standard term loans for equipment or expansion.

3. Instant Scenario Testing

Financial planning involves "What If" scenarios. What if I put more money down? What if I get a slightly better interest rate?

- Benefit: You can run dozens of scenarios in minutes without refreshing the page or recalculating manually.

4. Privacy and Security

Unlike lender-specific tools that require your email address or phone number (leading to spam calls), our Loan Calculator is purely a mathematical utility.

- Benefit: No data collection. No sales calls. Just pure data.

Step-by-Step Guide: How to Use the Tool

Using the Loan Calculator is intuitive, but knowing exactly what to input ensures the most accurate results.

Step 1: Input the Loan Amount (Principal)

Enter the total amount you plan to borrow.

- Tip: If you are buying a house for $400,000 and putting $50,000 down, enter $350,000 (the loan amount), not the purchase price.

Step 2: Input the Interest Rate

Enter the annual interest rate (APR) you expect to receive.

- Where to find this: Check current market rates, or look at your pre-approval letter.

- Note: If you don't have a quote yet, use the national average for your loan type to get a baseline estimate.

Step 3: Input the Loan Term

How long do you have to pay this back?

- Mortgages: Usually entered in years (e.g., 15 or 30).

- Car/Personal Loans: Often entered in months (e.g., 36, 48, 60, or 72 months).

Step 4: Analyze the Output

Once you hit calculate, focus on three distinct numbers:

- Monthly Payment: Can you fit this into your 50/30/20 budget?

- Total Interest Paid: This is the "wasted" money. Your goal should be to minimize this number as much as possible.

- Total Cost of Loan: The Principal + The Total Interest. This is the true price of the item you are buying.

Why You Need This Tool: 3 Critical Use Cases

Different borrowers have different needs. Here is how to apply this calculator to your specific situation.

Use Case 1: The Homebuyer (Mortgage Planning)

- The Problem: You are torn between a 30-year mortgage and a 15-year mortgage. The 30-year payment looks much more comfortable.

- The Solution: Use the calculator to compare the Total Interest. You will likely see that the 15-year mortgage saves you tens of thousands of dollars.

- Action: If the 15-year payment is too high, use the calculator to find a "sweet spot" by testing how extra payments on a 30-year loan affect the pay-off date.

Use Case 2: The Car Buyer (Auto Loan Reality Check)

- The Problem: Dealerships often focus on "monthly payments" to hide the total cost of the car. They might stretch a loan to 84 months just to get the payment under $400.

- The Solution: Plug the numbers into our calculator. You might discover that the 84-month loan results in paying $40,000 for a $30,000 car.

- Action: Use the tool to negotiate the Out the Door Price and the Interest Rate, rather than the monthly payment.

Use Case 3: The Debt Consolidator (Personal Loans)

- The Problem: You have $10,000 in credit card debt across three cards with varying high interest rates (e.g., 22%, 18%, 25%).

- The Solution: Check the estimated payment for a single $10,000 personal loan at a lower rate (e.g., 10%).

- Action: If the calculator shows the monthly payment is lower and the total interest is significantly less than what you are currently paying, consolidation is a green light.

Expert Advice: How to Get the Most Out of This Tool

As technical financial writers, we know that tools are only as good as the strategy behind them. Here are three "power moves" to maximize the utility of this calculator.

1. The "Extra $50" Test

After you calculate your base payment, try re-calculating with a slightly shorter term or a higher loan amount to simulate making extra payments.

- Insight: You will be shocked at how adding just $50 or $100 a month to your principal payment can shave years off a mortgage and save huge sums of interest.

2. Reverse Engineer Your Budget

Don't start with the car or house price. Start with your budget.

- If you know you can afford $400/month, use the calculator to tweak the Loan Amount until the monthly payment matches $400. This tells you exactly how much car or house you can afford before you even start shopping.

3. Factor in the "Hidden" Costs

Remember that this calculator estimates Principal and Interest (P&I).

- For Mortgages: Mentally add taxes, homeowner's insurance, and PMI (Private Mortgage Insurance). A $1,500 loan payment might actually be a $2,100 monthly housing expense.

- For Cars: Mentally add insurance and fuel costs.

Frequently Asked Questions (FAQ)

1. Does this calculator include property taxes and insurance?

By default, standard loan calculators estimate Principal and Interest only. Taxes and insurance vary wildly by location and provider. To get your full "PITI" (Principal, Interest, Taxes, Insurance) payment, you will need to add those estimated costs on top of the figure generated here.

2. How is the interest calculated?

This tool uses the standard formula for compound interest amortization. This is the industry standard for US mortgages and auto loans. It assumes a fixed rate over a fixed term.

3. Why is my first payment mostly interest?

This is how amortization works. The interest is calculated based on your remaining balance. At the start, your balance is high, so the interest charge is high. As you pay down the balance, the interest charge decreases, and more of your payment goes toward principal.

4. Can I use this for credit card payments?

Technically, yes, to estimate a payoff date. However, credit cards use "revolving" credit with minimum payment calculations that differ from "installment" loans. This tool is best suited for fixed-term loans like mortgages, autos, and personal loans.

5. Will using this calculator affect my credit score?

Absolutely not. This is a simulation tool. It does not pull your credit report, require your Social Security number, or alert bureaus. You can run as many calculations as you like risk-free.

Conclusion: Stop Guessing, Start Calculating

Financial freedom isn't about how much money you make; it's about how much money you keep. Lenders are in the business of selling you money, and their profit is the interest you pay.

By using our Loan Calculator, you shift the power dynamic. You move from a passive borrower hoping for a good deal to an informed buyer who understands the true cost of debt. Whether you are looking to buy a home, drive a new car, or simply organize your finances, clarity starts here.

Ready to see the numbers? Scroll up, enter your details, and take control of your financial future today.